Medicare Supplement insurance premiums generally increase each year due to several factors, including inflation, rising healthcare costs, and the age-attained pricing structure used by many insurance companies. In addition, Medicare itself often raises deductibles annually, which can also contribute to premium increases since many supplement plans help cover those deductibles.

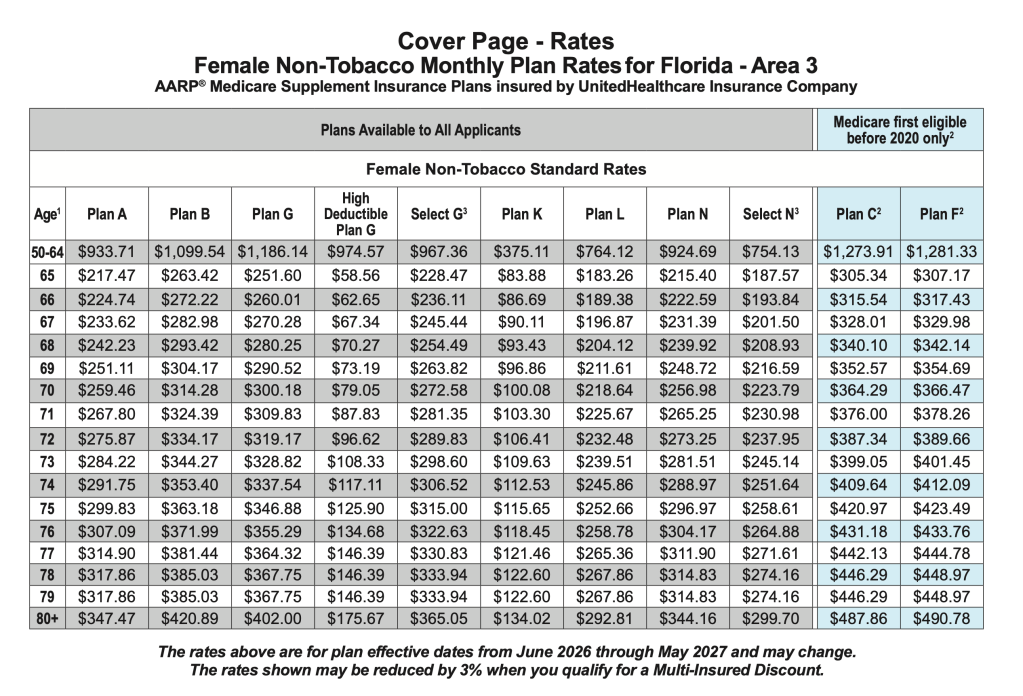

This year, UnitedHealthcare has announced average premium increases of approximately 14% for women and 20% for men across several of its Medicare Supplement plans. For example, a 65-year-old female non-tobacco user in Area 3 enrolled in Supplement Plan G previously paid $218.39 per month. Beginning June 1, that monthly premium will increase to $251.60.

So, what factors truly contribute to these premium increases?

One major factor is the continued rise in healthcare costs and inflation. As the cost of medical care increases, insurance companies must pay more to cover claims for policyholders. To offset these higher claim expenses, insurers often raise monthly premiums to maintain financial stability. Insurance operates by pooling premiums from all members, meaning individuals who rarely use their coverage still contribute toward the claims expenses of others within the plan.

Insurance companies also generate revenue by investing premium income into financial assets such as stocks, bonds, and real estate. These investments help support claim payments and reduce reliance solely on incoming premiums. However, rising healthcare costs remain one of the primary drivers behind annual premium increases.

Another contributing factor is age-attained pricing. Like many Medicare Supplement providers, UnitedHealthcare uses an age-attained pricing model, meaning premiums are based on the insured’s current age. Generally, premiums are lower at age 65 and increase as the policyholder gets older. For example, a female non-tobacco user in Area 3 enrolled in Supplement Plan G would pay $251.60 at age 65, while that same plan is projected to cost $337.54 at age 74 in 2026.

This pricing structure reflects the increased likelihood that individuals will utilize more healthcare services as they age. While many people remain healthy well into retirement, healthcare usage and the potential for chronic conditions typically increase over time, resulting in higher costs for insurers.

Another factor affecting premiums is the annual increase in Medicare deductibles. Certain Medicare Supplement plans, such as Plans C and F, cover the Medicare Part B deductible. In 2026, the Medicare deductible increased from $257 to $283, a $26 increase from the previous year. While this may appear minimal on an individual level, the impact becomes much larger when spread across an entire pool of policyholders.

For example, if 100 members are enrolled in a plan that covers the Medicare deductible, the supplement carrier would need to absorb an additional $2,600 in deductible expenses collectively. As Medicare deductibles continue to rise, supplement plans covering those costs may also need to increase premiums accordingly.

Lastly, insurance companies closely monitor something called the loss ratio. The loss ratio measures how much an insurance company pays out in claims compared to how much it collects in premiums. The formula is:

For example, if a company pays $1,000,000 in claims while collecting $2,000,000 in premiums, the company would have a 50% loss ratio. If a carrier’s loss ratio rises above a sustainable level, premium increases may be necessary to maintain financial balance and continue meeting future claim obligations.

If you would like to learn more about the Medicare Supplement plans available in your area or have questions about these recent changes, contact Streamline Insurance Consultants or speak with an experienced local agent or broker. If you are new to Streamline Insurance Consultants, please visit our Contact Us page and complete the form so we can connect with you and help guide you through these often confusing Medicare changes.

If you would like a copy of the new supplement book for 2025 please let us know!

Leave a comment